The Fed has learnt from the past

Fed officials have been signalling the change in monetary policy for months in advance. Obviously, the people at the top have learned the right lessons from 2013. The then Fed Chairman Ben Bernanke had caught the markets on the wrong foot with his announcement that he wanted to reduce bond purchases. This ended up in an episode later named "taper tantrum".

Financial market participants also reacted calmly to the prospect of key interest rate hikes in the coming year, as expected by the Fed's governing body. Yields for shorter maturities of sovereign bonds rose sharply, but yields at the longer end of the yield curve fell slightly. This has flattened the curve, which in the past was often a signal of emerging concerns about a recession. This reflects the supply shortages in international trade, which have still not been resolved and thus increase short-term economic risks. But there are no widespread recession fears. Companies' order books are full and consumers are still confident and spend money. Therefore, we consider the flattening of the yield curve to be only a temporary phenomenon.

On the stock markets, too, the mood is anything but glum at the moment. The markets have recovered from their interim setback and a whole series of sentiment indicators show a renewed increase in risk appetite. This positive mood is fuelled by good to excellent company figures for the third quarter.

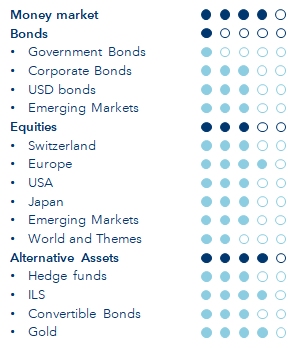

Against this backdrop, the Investment Committee has decided to stick to the current tactical positioning. In equities, we have a preference for the European market and for Chinese consumer stocks.

Add the first comment