Use dividends as a guide

Although the effects and containment of the coronavirus pandemic are proving to be much more complex than previously assumed, there are also signs of solutions. Thanks mainly to the achievements of the digital economy and teleworking, the economic damage suffered by listed companies over the past year was less drastic than had been feared. But there are clear regional differences in this regard: countries like China and the USA, where the exchanges are home to an above-average number of modern information technology stocks, have fared much better. China’s stock market is also benefiting from the disproportionately high demand for goods from online retailers. However, technology stocks are traditionally not generous dividend payers, as they prefer to invest a large share of their profits in their future growth rather than distributing that money to shareholders.

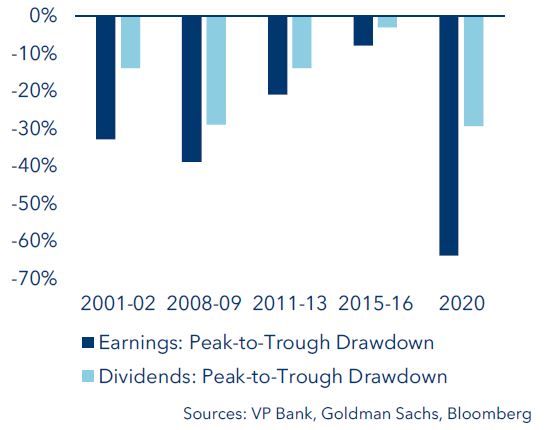

Europe, on the other hand, is more focused on traditional industry and services, companies that generally pay above-average dividends. So here, the restrictions on mobility as well as the prevalence of financial stocks have resulted in relative underperformance due to the adverse economic circumstances and related uncertainties. Nonetheless, even though the decline in profits has been exceptionally high compared to previous crises, many companies are still paying their accustomed dividends in full or at least partially. In the latter instance, some of the initially suspended profit distributions were actually made up for later in the year.

EURO STOXX 50: Profits and dividends in crisis years

Emotional market participants

The outbreak of the pandemic in Europe and America triggered intense fears and a precipitous drop in share prices, especially once the initial containment measures were announced. But after a surprisingly short amount of time, an impulsive knee-jerk recovery set in – and that rally has persisted. Major markets such as the USA and China have recovered by 76% and 85% respectively, even reaching new highs along the way. Shares in Europe have risen by a good 58% from their March 2020 lows, with the defensive Swiss equity market lagging the pack by recording a mere 40% gain for the same period. The dominant themes for investors have been digitalisation and automation, environmental sustainability, and hopes for the economic recovery of companies hard hit by the crisis. The sometimes dramatic short-term price swings of late suggest that – as is so often the case – investors’ profit expectations have now gotten ahead of reality. By the same token, this tunnel vision on only a few sectors also creates clear discrepancies, as reflected in the diverging dividend expectations for the key US and European share indices.

Diverging dividend expectations (indexed)

This underscores the clear message sent by stable dividend payments – in the US, the expectations are almost back to where they were last year at this time. But if one links this to the earnings outlook, those expectations appear to be too low for Europe.

For the current business year, analysts expect that profit distributions in the USA, Switzerland and emerging markets will be at or above the level of 2019. For Europe, though, the forecast is 18% lower. Moreover, the estimates for 2022 still show a shortfall of 9%. This implies significantly weaker relative earnings growth, which is totally incongruent with current earnings expectations.

Summary

In an environment of highly selective and concentrated market price movements, stable dividend pay-outs offer guidance on the financial strength of companies. But despite their reliable distributions, stocks of this nature continue to be neglected in the US and Swiss markets and are trading at too high a discount in Europe. This affords medium- to long-term investors a good opportunity to acquire shares of high-quality companies at attractive prices.

For more information please contact your client advisor.

Important legal information

This document was produced by VP Bank AG (hereinafter: the Bank) and distributed by the companies of VP Bank Group. This document does not constitute an offer or an invitation to buy or sell financial instruments. The recommendations, assessments and statements it contains represent the personal opinions of the VP Bank AG analyst concerned as at the publication date stated in the document and may be changed at any time without advance notice. This document is based on information derived from sources that are believed to be reliable. Although the utmost care has been taken in producing this document and the assessments it contains, no warranty or guarantee can be given that its contents are entirely accurate and complete. In particular, the information in this document may not include all relevant information regarding the financial instruments referred to herein or their issuers.

Additional important information on the risks associated with the financial instruments described in this document, on the characteristics of VP Bank Group, on the treatment of conflicts of interest in connection with these financial instruments and on the distribution of this document can be found at https://www.vpbank.com/legal_notice_en

Add the first comment