The next round of catch-up effects is already waiting

One-month gasoline contracts in Europe have increased more than sixfold within a year. This is causing a stir and has fuelled inflation concerns. The higher energy bills also threaten to depress consumer and business sentiment. The latter are already suffering from material shortages and supply bottlenecks. Not surprisingly, the spectre of stagflation, i.e. the ominous combination of a stagnating economy and rising inflation, has been making the rounds recently. In our view, however, the danger of a stagflationary development is low. In the short term, inflation rates will remain high and the growth figures for the fourth quarter will indeed be weaker due to the shortage of materials. But already at the beginning of next year, growth momentum should pick up again. This is supported by the empty warehouses and full order books in industry. When the material and supply situation begins to ease, the next round of catch-up effects is already waiting.

We also expect inflation rates to fall again. A harbinger of this is the development of commodity prices for metal, copper or nickel. After the strong increase at the beginning of the year, these have already fallen back significantly.

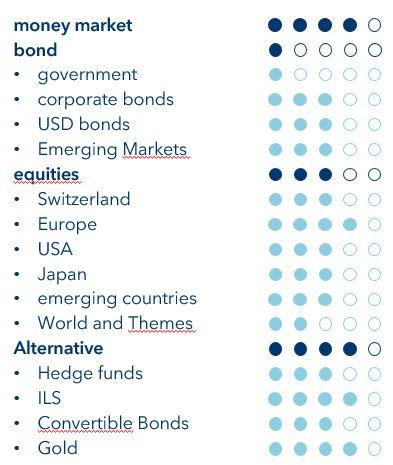

Against this background, we confirm our current portfolio positioning. We continue to exercise restraint with government bonds. On the other hand, we consider gold and insurance-linked securities to be interesting from a tactical point of view. In equities, we are sticking to the strategic quota and tactically focusing on European equities and Chinese consumer stocks.

Add the first comment